Inflation volatility and inflation in the wake of the great recession

- PDF / 1,077,614 Bytes

- 19 Pages / 439.37 x 666.142 pts Page_size

- 37 Downloads / 294 Views

Inflation volatility and inflation in the wake of the great recession Semih Emre Çekin1

· Victor J. Valcarcel2

Received: 1 February 2017 / Accepted: 6 May 2019 © Springer-Verlag GmbH Germany, part of Springer Nature 2019

Abstract A reduced-form investigation reveals that the relationship between the level of inflation and its volatility in the USA may not have been monotonic. This paper quantifies a reversal of the relationship by considering linear and nonlinear estimation methodologies on the trend and volatility of inflation. Our findings suggest that the spikes in inflation volatility in the period after 2008 are related to transitory, rather than permanent movements in inflation, suggesting that the US Great Moderation period may be merely on hold, rather than over with. Keywords Inflation volatility · Markov switching · Mixed-frequency regressions · GARCH · MIDAS JEL Classification E30 · E31 · E65

1 Introduction The US Great Recession of 2008 and its aftermath have sparked new debates surrounding the conduct of monetary policy, viz. inflation dynamics. An extremely loose monetary policy leading to the zero-lower-bound (ZLB) in the policy rate, the perception of a threat of deflation, and headwinds in economic activity both in the USA and

We wish to thank conference participants at the 2nd Annual Society for Economic Measurement (SEM) conference in Paris, France. All standard disclaimers apply.

B

Semih Emre Çekin [email protected] Victor J. Valcarcel [email protected]

1

Faculty of Economic and Administrative Sciences, Turkish-German University, 34820 Istanbul, Turkey

2

School of Economics, Political and Policy Sciences, University of Texas at Dallas, GR.2.516, Richardson, TX 75080, USA

123

S. E. Çekin, V. J. Valcarcel

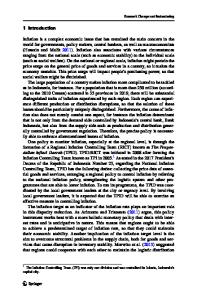

Fig. 1 US CPI inflation rates: 1965:m1–2018:m3

in Europe have led some economists to propose raising the inflation target to higher levels than the 2% that most Central Banks currently pursue.1 While Blanchard et al. (2010) and Ball (2013) discussed the possibility of raising the target to 4%, Bernanke (2010) suggested that such an option would entail greater costs than benefits, including potential detriment to the credibility of Federal Reserve. In addition to the well-known adverse effects of deflation, these discussions have implications for the relationship between inflation and its volatility. A cursory inspection of US inflation dynamics, as shown in Fig. 1, suggests that the Great Inflation period of the 1970s came hand in hand with high inflation volatility. Conversely, in the aftermath of the US Financial Crisis of 2007, some measures of inflation volatility increased at a time when inflation levels were low (see lower panel of Fig. 1) and inflation expectations seemed well-anchored. Typical investigations of inflation dynamics typically incorporate long-run and short-run behaviors. While the long-run, or trend component, is generally thought to be in the realm of attention of a central bank and of prime concern in deliberations of monetary policy, the short-

Data Loading...