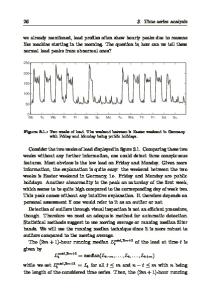

Introduction to Modern Time Series Analysis

This book presents modern developments in time series econometrics that are applied to macroeconomic and financial time series, bridging the gap between methods and realistic applications. It presents the most important approaches to the analysis of time

- PDF / 3,687,658 Bytes

- 325 Pages / 439.37 x 666.14 pts Page_size

- 18 Downloads / 809 Views

For further volumes: http://www.springer.com/series/10099

.

Gebhard Kirchgässner • Jürgen Wolters Uwe Hassler

Introduction to Modern Time Series Analysis Second Edition

Gebhard Kirchgässner SIAW-HSG University of St. Gallen St. Gallen Switzerland

Jürgen Wolters Institute for Statistics and Econometrics FU Berlin Berlin Germany

Uwe Hassler Applied Econometrics and International Economic Policy Goethe University Frankfurt Frankfurt Germany

ISSN 2192-4333 ISSN 2192-4341 (electronic) ISBN 978-3-642-33435-1 ISBN 978-3-642-33436 -8 (eBook) DOI 10.1007/978-3-642-33436-8 Springer Heidelberg New York Dordrecht London Library of Congress Control Number: 2012950003 © Springer-Verlag Berlin Heidelberg 2013 This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmission or information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. Exempted from this legal reservation are brief excerpts in connection with reviews or scholarly analysis or material supplied specifically for the purpose of being entered and executed on a computer system, for exclusive use by the purchaser of the work. Duplication of this publication or parts thereof is permitted only under the provisions of the Copyright Law of the Publisher’s location, in its current version, and permission for use must always be obtained from Springer. Permissions for use may be obtained through RightsLink at the Copyright Clearance Center. Violations are liable to prosecution under the respective Copyright Law. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. While the advice and information in this book are believed to be true and accurate at the date of publication, neither the authors nor the editors nor the publisher can accept any legal responsibility for any errors or omissions that may be made. The publisher makes no warranty, express or implied, with respect to the material contained herein. Printed on acid-free paper Springer is part of Springer Science+Business Media (www.springer.com)

Preface to the Second Edition

In preparing this second and enlarged edition, a third author has joined the team. Still, the scope of the book has not changed. We try to provide a rigorous understanding of the theory and methods of univariate and multivariate time series analysis. At the same time, the main objective is the development of empirical skills with a special emphasis on the link to economic applications. Therefore, we strengthened the specific feature of our book that now contains 63 examples, most of the

Data Loading...